The view from the EU

Copyright: GettyImages

Fit for 55 notes that a combination of measures is required to tackle rising emissions in road transport. Stronger CO₂ emissions standards for both cars and vans will accelerate the transition to zero-emission mobility by requiring average emissions of new cars to come down by 55% from 2030 and 100% from 2035 compared to 2021 levels. As a result, all new cars registered from 2035 must be zero-emission.⁹

To ensure that drivers are able to charge or fuel their vehicles at a reliable network across Europe, the revised Alternative Fuels Infrastructure Regulation¹⁰ will require member states to expand charging capacity in line with zero-emission car sales, and to install charging and fuelling points at regular intervals on major highways: every 60 km for electric charging and every 150 km for hydrogen refuelling.

As technological progress in the electrification of two/three-wheelers, buses, and trucks advances and the market for them grows, the deployment of EVs is expanding significantly.

At the same time, the increased appetite is encouraging new investment in everything from batteries and vehicle design, to smart and fast charging infrastructure.

Ambitious policy announcements have been critical in stimulating the EV rollout in major vehicle markets. In its Global EV Outlook 2021, the IEA says that near-term efforts must focus on continuing to make EVs competitive and gradually phasing out purchase subsidies, to shift to policy approaches that rely more on regulatory and other structural measures, including differentiated taxation of vehicles and fuels, based on their environmental performance, for example.¹¹

This is sending clear, long-term signals to the automotive industry and consumers that in the transition to net zero, EVs represent an important step.

1

The role of the Paris Agreement

The International Renewable Energy Agency (IRENA) is also emphatic about the role electric vehicles can play in helping to achieve global carbon emissions reduction targets set under the Paris Climate Change Agreement.

It projects that $2 trillion in annual investment will be required to achieve the Paris goals in the coming three years, and says eMobility has a major role to play in this regard. IRENA’s transformation pathway estimates that 350 million EVs will be needed by 2030, kick-starting developments in the industry and influencing share values as manufacturers, suppliers and investors move to capitalise on the energy transition.¹²

2

A growing market

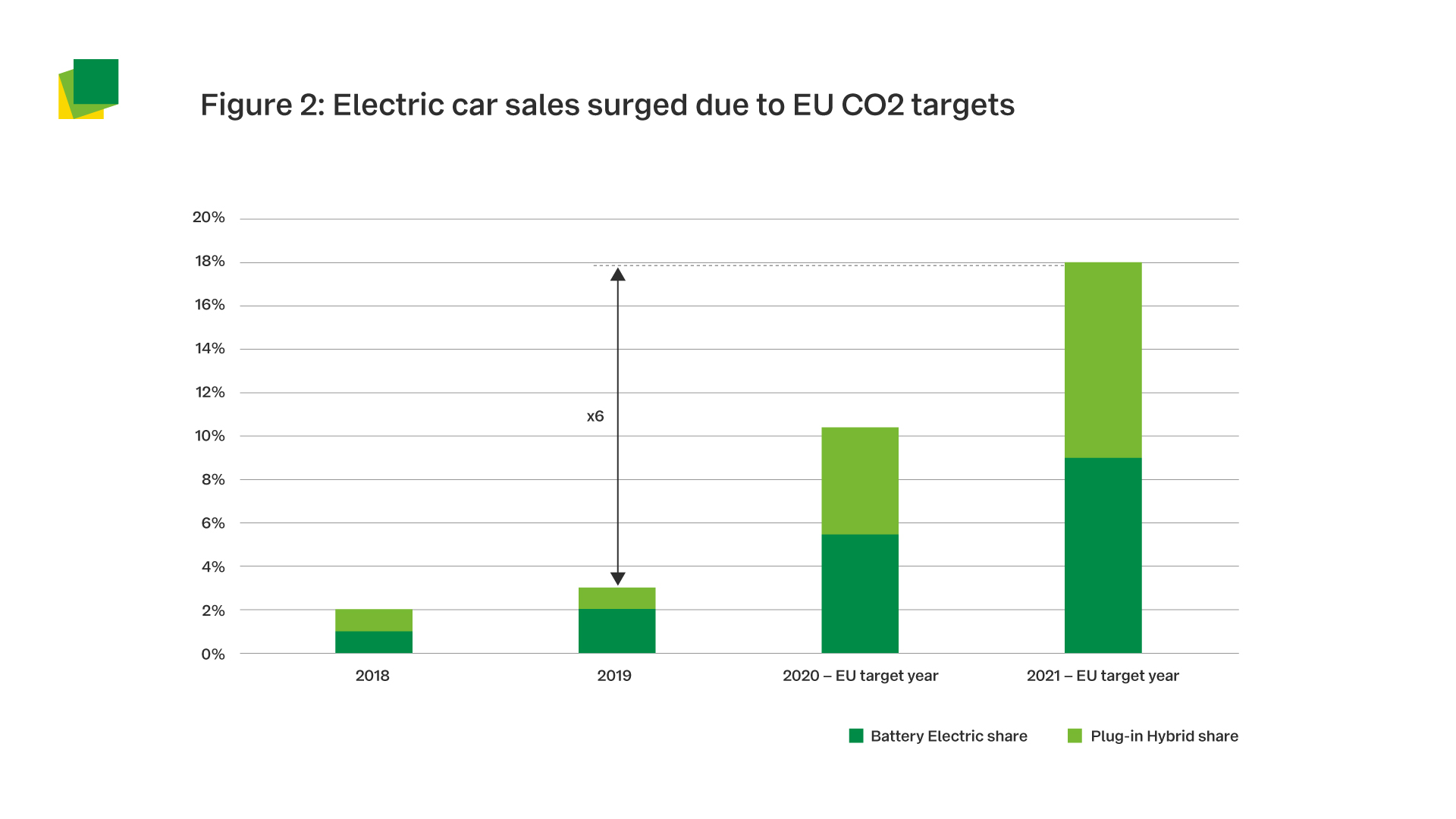

Research shows that encouragingly, eMobility grew considerably in 2021 as plug-in¹³ vehicles made up 18% of the European market, compared to only 10.5% in 2020 (see figure 2), with most of the manufacturers exceeding the new targets.

Battery-electric vehicles (BEV) accounted for 9.1% of passenger car sales in the EU27 (5.4% in 2020), while plug-in hybrids (PHEV) reached 8.9% of the market (5.1% in 2020)¹⁴. Their combined sales share has multiplied by six since 2019 in the EU27 thanks to the EU car CO₂ standards.¹⁵

More than 1.7 million plug-ins were sold in the EU27 in 2021 (more than 2 million including the UK), which increased the number of EVs on European roads to 5.5 million.¹⁶

Germany led the way in EV sales in Europe. In 2021, 356,000 BEVs and 325,000 PHEVs were sold, up from 194,000 and 200,000 respectively in 2020. For context, France sold 162,000 BEVs and 141,000 PHEVs in 2021. The UK sold 191,000 BEVs and 114,000 PHEVs in the same year.¹⁷

Source: Transport & Environment

Considering countries outside of the European Union, Norway has the largest plug-in segment share with almost 85% end of 2021, followed by Iceland.¹⁸

According to ‘Plugged-in’: T&E’s market watch, one in every 11 cars sold in the EU in 2021 was fully electric as EV sales continued to be boosted by EU CO₂ targets.