What good is an EV without a charge point? Supporting the growth in the EV charging market

As of end of 2020, 225,000 public charging points exist across the EU, says the European Alternative Fuels Observatory (EAFO). More than 60,000 new charging points were installed in 2020, expanding the network by 37%. In particular, the number of fast charging stations whose power is over 22 kW increased by 67%, growing their share of all charging points from 9.2% in 2019 to 11.3% in 2020.²⁴

However, it notes that public infrastructure development did not fully match the growth of electric mobility. The total number of plug-ins on the road nearly doubled in the EU, from 1,101,000 EVs in 2019 to 2,111,000 EVs in 2020. As a result, the ratio of plug-ins per charging point jumped from 6.7 to 9.4. This ratio is very close to the one recommended by the European Commission of one public charger for every 10 EVs, indicating that the public charging supply is maturing. However much more needs to be done to match the future uptake of eMobility, thanks to an ambitious revision of the Alternative Fuels Infrastructure Directive (AFID), included in the Fit for 55 package.²⁵

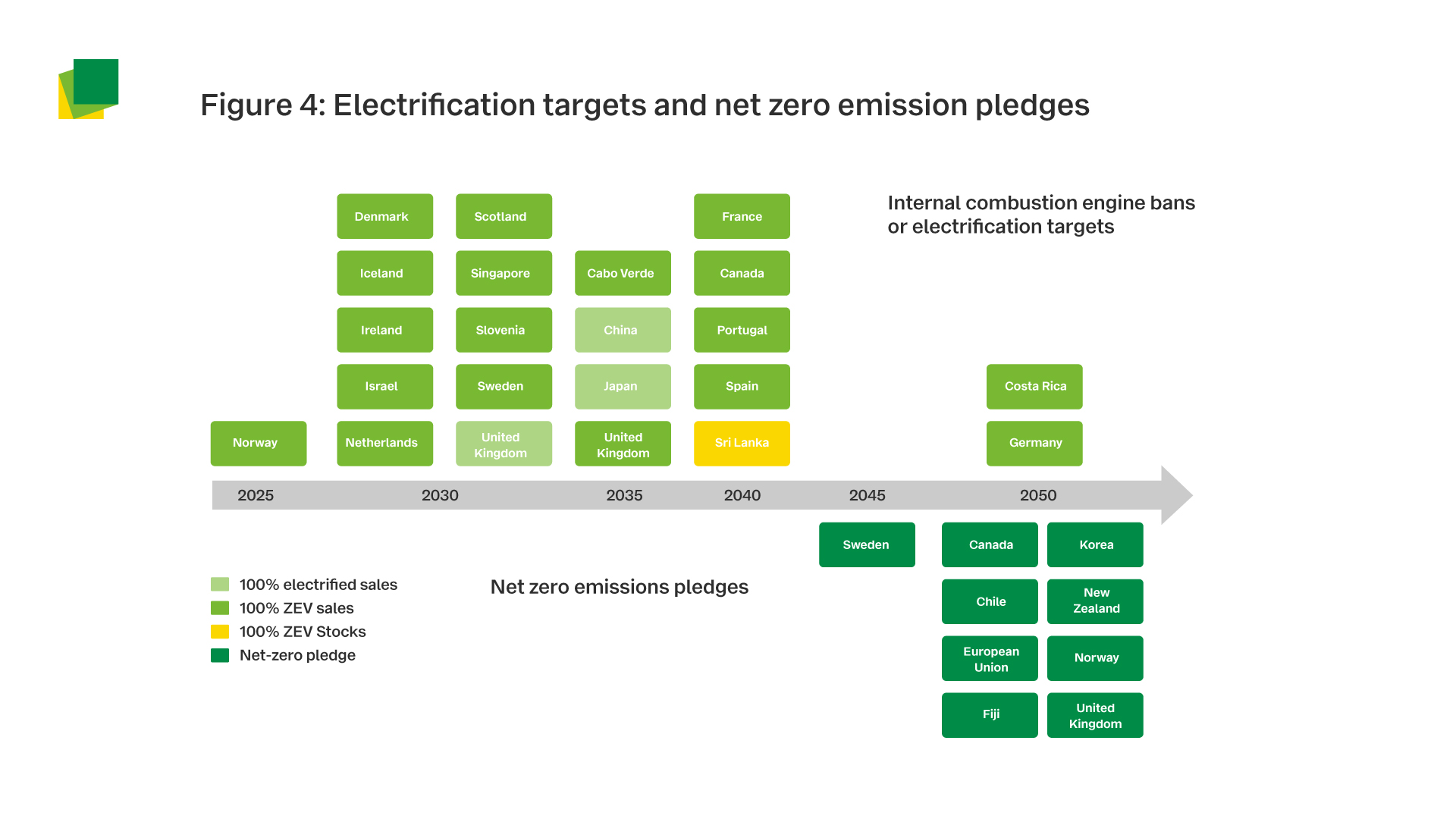

As a result of the climate and energy crisies, electrification targets and net zero emission pledges have become more and more ambitious (see figure 4). To keep up with the upcoming electric surge the European Union's infrastructure framework needs to prioritise electric charging and be in line with the increasing demand for public and private charge points, according to Transport & Environment (T&E).

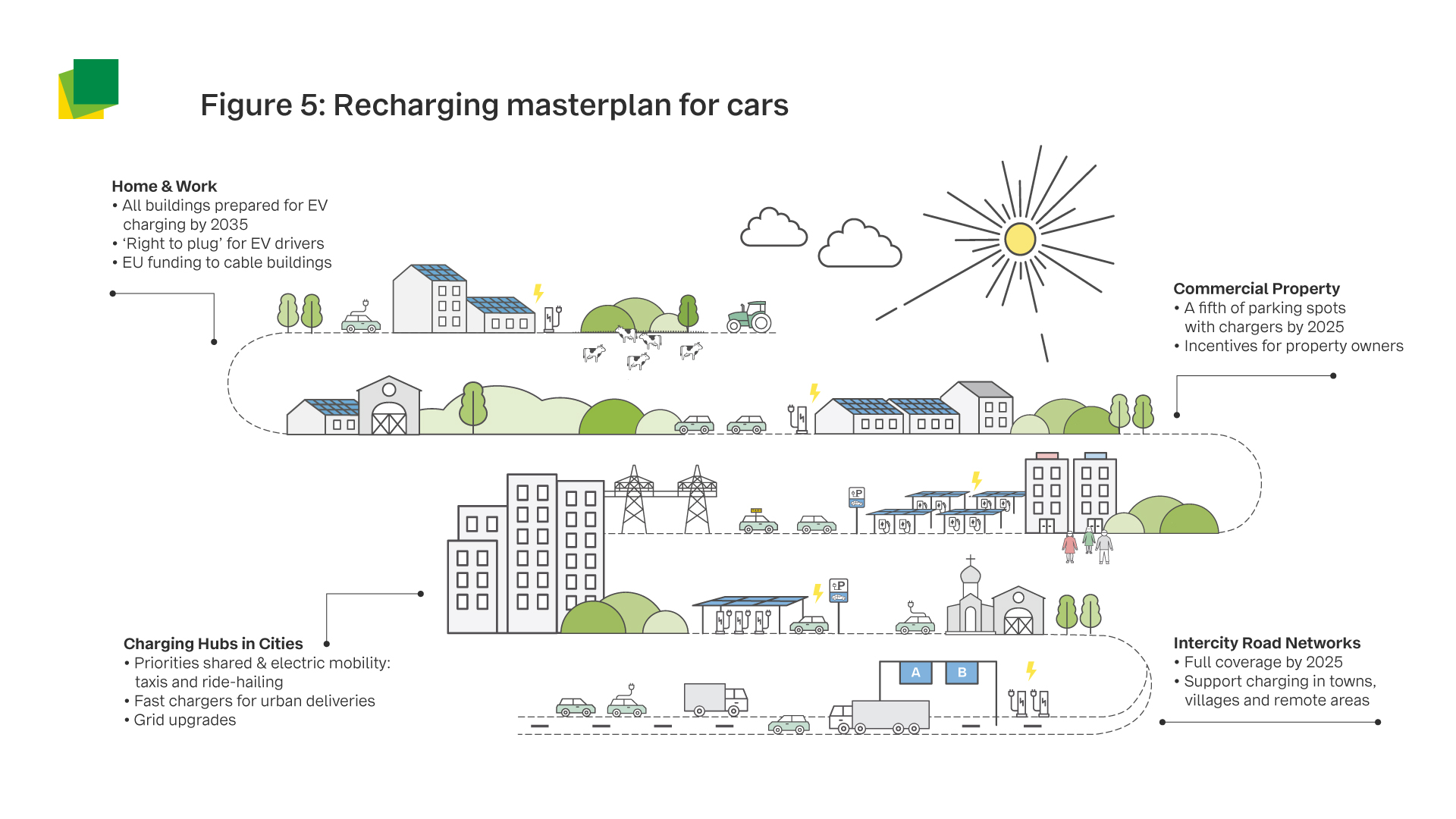

It notes that a new EU policy framework for alternative fuels infrastructure and funding mechanisms being discussed in the European Green Deal are the two cornerstones required to deliver an ambitious EU recharging infrastructure masterplan (see figure 5).²⁶

It’s generally acknowledged that further effort will be needed to ensure seamless and reliable charging within and across countries for drivers, both in terms of infrastructure and technology. New European regulation would create a strong foundation and encourage timely harmonisation across borders. The charging deployment should be fairly spread across Europe to ensure all Europeans get the same chance to shift to zero-emission mobility.

T&E’s research suggests that 1.3 million public charge points will be needed EU-wide in 2025 and close to 3 million in 2030. In total, this would require investment of €1.8 billion in the year 2025, equating to 3% of the EU’s annual investment in road transport infrastructure.

There is great potential for creating the right charging infrastructure in cities, given the need - and opportunity - to reduce the dependency on private cars. A sustainable transition featuring the use of charging solutions for a growing fleet of shared cars, electric taxis and ride hailing services, as well as delivery electric trucks and vans seems an obvious way forward. Investment will inevitably be required, not only to create the infrastructure, but also to ensure there is sufficient, robust grid capacity.

Source: IEA

Overall, the shift to EVs will create a multi-billion euro market opportunity for European industry in the grid works and the manufacturing, installation, and maintenance of the charging equipment. The new European Commission and its EU Green Deal has a key role to play in making the transition to eMobility a success. Not only is this transition essential to face the climate emergency, it will also serve as a building block for the EU’s transition towards a zero emission economy while boosting EU competitiveness.

Source: Transport & Environment

To drive electric is good, but to drive renewable is better

Growth in the EV market and expansion of charging point infrastructure all seems like good news. But while these two elements are undoubtedly signs of positive progress, what about the power sources used to keep EVs on the road?

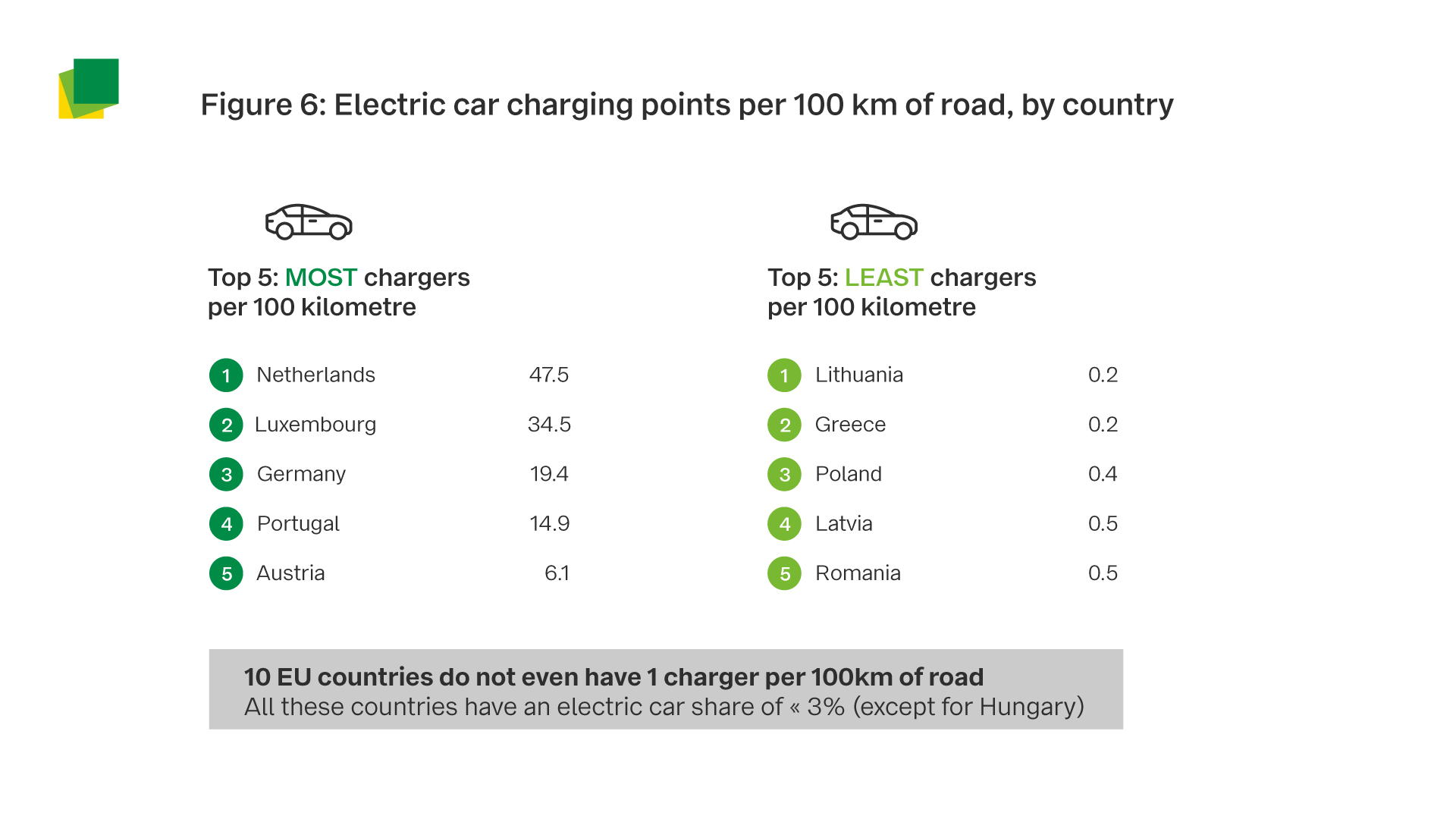

There is a critical third ingredient here that’s required if EVs are really going to make the maximum contribution to cutting carbon emissions – and that is the fuel source. If the electricity being used is derived from fossil fuels, then eMobility remains an imperfect solution. And while some countries in Europe already have comparatively comprehensive charging infrastructure in place, many do not (see figure 6). There are, however, promising initiatives to further improve in this matter.

In Germany, for example, the Federal Foreign Office commissioned ‘T4<2°– Transport for under two degrees’– a 2020 global foresight study on the decarbonisation and transformation of the transport sector to identify challenges and opportunities for a sustainable, low-carbon transport sector in Germany and beyond.²⁷

The findings provide decision-makers with a clear vision and specific recommendations on how to achieve decarbonisation of the sector and orchestrate international efforts for a global transport system transformation.

Source: ACEA

There is the additional factor that a great deal of energy is consumed in the production of EV batteries. This results in CO₂ emissions in the countries of manufacture (primarily China, Japan, and South Korea). As a result, EVs have a larger carbon footprint than conventional vehicles when it comes to the manufacturing process. To make up for this disadvantage, an EV must be driven for several thousand kilometres with low-carbon power.

In spite of these caveats, EVs are currently overall more ecological than their conventional counterparts. This ecological advantage will continue to grow in the future as industry taps into opportunities for reducing carbon emissions in both power generation and vehicle production.

Research by Agora suggests that the carbon footprint of batteries can be more than halved in the coming years thanks to more efficient production methods, improved cell chemistry and energy density, and the use of green electricity as a production output.²⁸