Introduction to eMobility in Europe

The transport sector continues to be one of the biggest contributors to global carbon emissions, and accounted for 37% of CO₂ emissions from end-use sectors in 2021.¹

Around the world, road vehicles account for nearly three-quarters of transport CO₂ emissions, and while the COVID-19 pandemic has resulted in a slow-down, emissions are still set to rise.²

However, electrifying transport could dramatically reduce emissions by 77% in 2050, with an additional 7-10% achievable if adoption of electric vehicles (EVs) were to accelerate.³

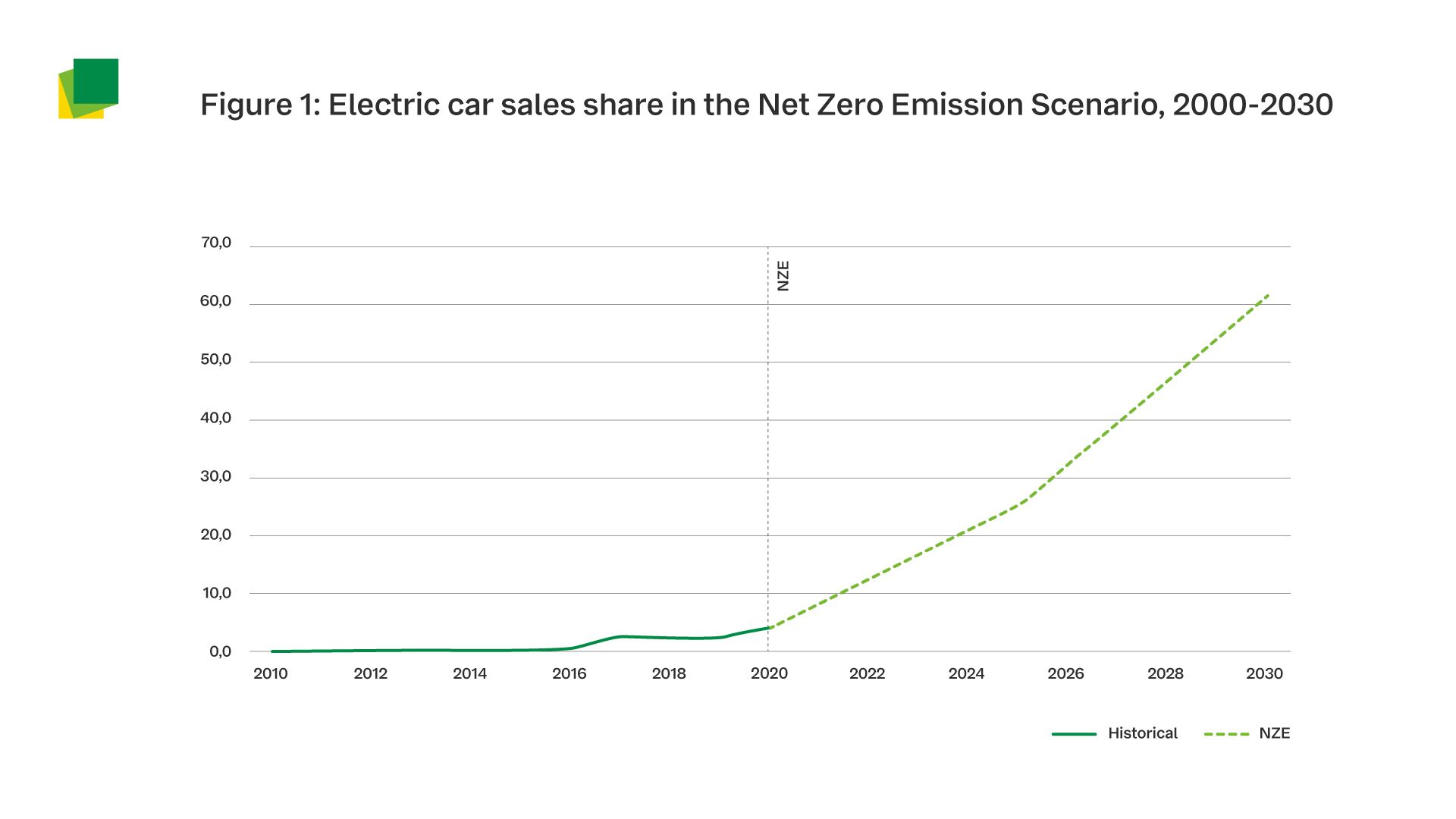

The good news is that there has been increasing global take-up of EVs over the past decade. The International Energy Agency (IEA) reported that sales of EVs topped 6.6 million in 2021 – more than tripling their market share from just two years previously.⁴ Their Net Zero Emissions Scenario sees an electric car fleet over 300 million in 2030 and electric cars representing 60% of new car sales globally (see figure 1).⁵

While the global scale of EV growth is important for context, this white paper is focusing on Europe, the largest EV market after China. The EU’s recent Fit for 55 package aims for a 55% drop in CO₂ emissions from new cars and 50% from new vans by 2030. By 2035, emissions from these vehicles will be cut completely and all new vehicles registered in Europe must be zero emission, if everything goes to plan.⁶

eMobility as a rapidly developing technology has the potential to become Europe’s sustainable ride towards a greener future. However, while it offers many opportunities, it also faces a variety of challenges that must be addressed to make the switch from gas-guzzler to EV. This paper serves as a roadmap for this journey.

Source: IEA

While they can’t do the job alone, electric vehicles have an indispensable role to play in reaching net-zero emissions worldwide.